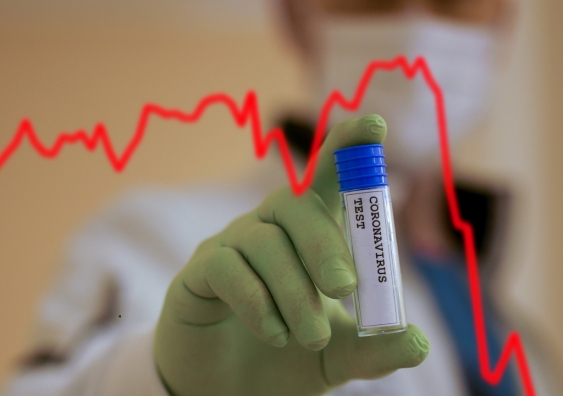

3 useful things to know about fear economics (and how to contain it)

Volatility in stock markets has increased dramatically thanks to the fear around COVID-19. Investors should therefore consider these three questions to get a better grip of the situation, says a UNSW expert.

Published on the 24 Mar 2020 by James Doran