Going up. Monday showed what the market thinks of Morrison

Monday's share market surge was a pure as any a test of what the market thought of the election results.

Published on the 21 May 2019 by Mark Humphery-Jenner

Monday's share market surge was a pure as any a test of what the market thought of the election results.

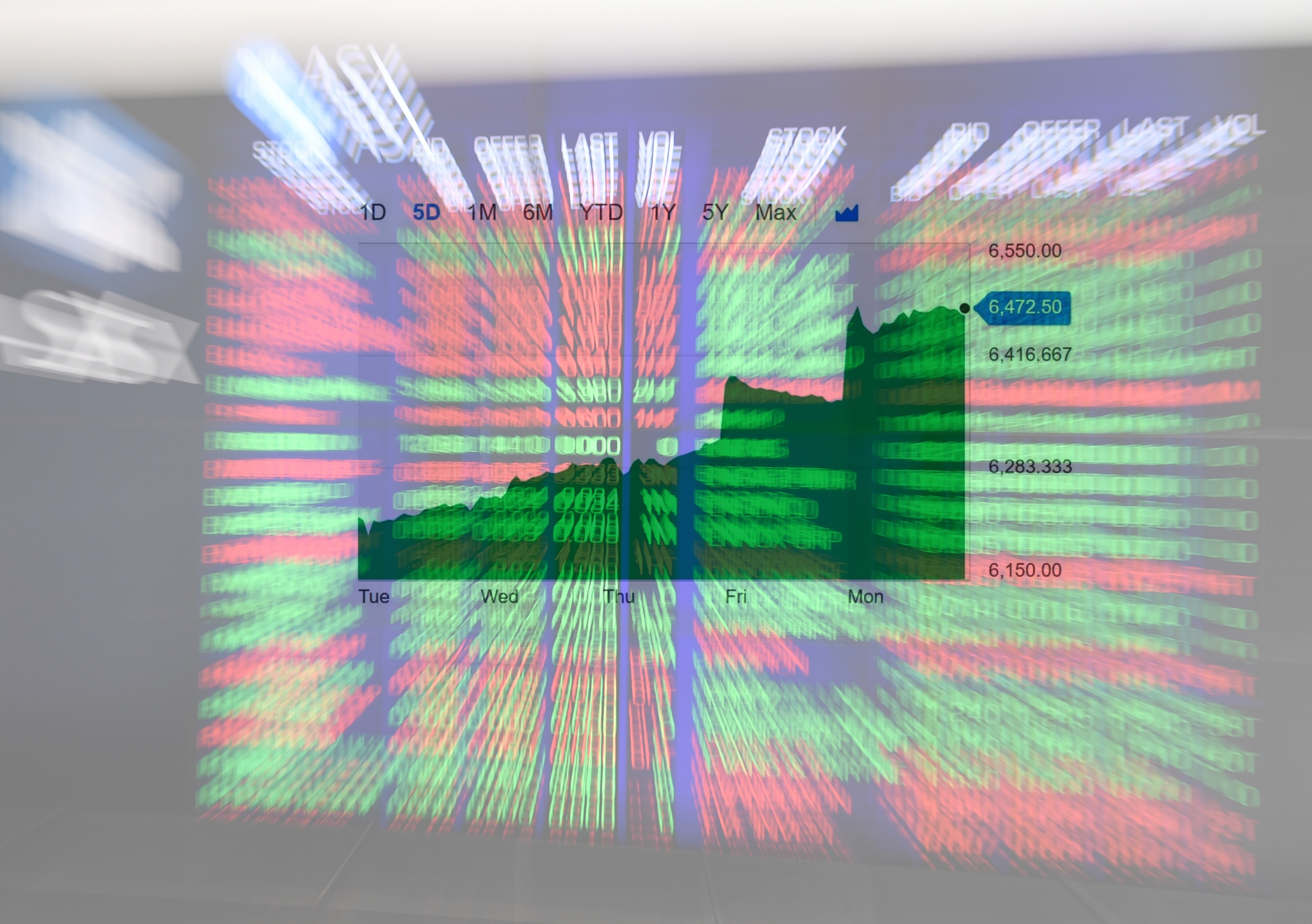

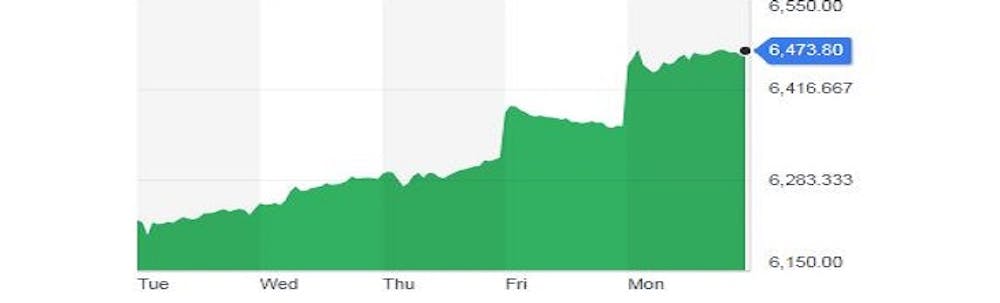

The coalition’s shock victory pushed up the S&P ASX 200 by 1.7% – the biggest one-day surge since Kevin Rudd was elected prime minister in 2007.

The ASX 200 measures the price of Australia’s 200 biggest public companies. The jump pushed up the value of shares across the entire market by A$33 billion. The price of one of the banks jumped 9%.

All of the polls leading up to the election had had Labor ahead, with Labor apparently widening its lead in the final few days.

Punters placing bets also overwhelmingly favoured Labor. Sportsbet was so confident of a Labor victory, it paid out bets on Labor early.

Which Monday’s jumped was the reaction to a surprise.

The market had been expecting a Shorten victory. It had to suddenly reprice after discovering it was a Morrison victory.

It’s pretty clear that the jump didn’t reflect anything else, for two reasons:

it is surprises rather than what was already known that moves markets, because everything else is already priced in, and the coalition victory was the only big surprise between the close of business on Friday and the start of trade on Monday

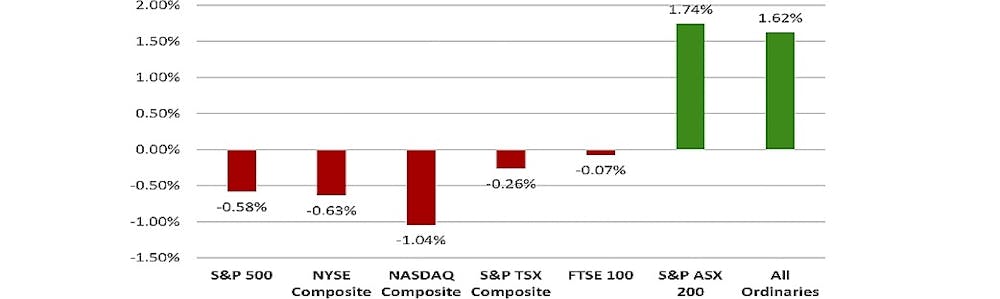

we are able to compare the ASX movements with those on other markets ahead of Monday’s opening. The ASX normally follows other markets unless there is a clear (local) reason to do otherwise. In this case, the indexes in the United States, Britain and Canada had all fallen in their most recent sessions before Monday’s opening. By contrast, the Australian indexes jumped sharply, suggesting a very strong positive reaction to only big piece of local news since the foreign markets closed

Others down, Australia up

It’s hard to be sure, and different government policies affect different industries differently. But there are common threads:

Property effects: Labor’s capital gains tax and negative gearing tax policies might have hurt property prices.

The prospect of prices somewhat stronger than they might have been means the prospect of a softening in the decline in construction, and better employment prospects than otherwise, which would mean better economic growth than otherwise. Stronger property prices bolster consumer confidence, supporting spending indirectly, and can also support it directly making it easier for consumers to tap into equity in their homes.

Tax factors: The market generally reacts well to tax cuts. This was the case with Trump’s tax cuts in the United States, in part because of the expectation that they would boost the economy. The market generally dislikes tax increases. While it is not clear whether the Coalition’s promised longer-term tax cuts will materialise, the Coalition has plans for longer-term tax cuts that Labor didn’t.

Labor’s dividend imputation policy would have harmed retirees’ incomes. With it off the agenda they can have the confidence to spend and hold shares that they had before.

Banking and finance: The coalition is generally seen as more concilliatory towards the banking sector, being reticent to impose major penalties after the banking royal commission, and reluctant to hold it in the first place. The price of the big four banks surged on Monday. The Commonwealth Bank jumped the least, 6.3%. Westpac jumped 9.2%.

Mining and energy: Labor was perceived as hostile to mining and resource companies. Several recorded strong price gains. Its seeming reluctance to acknowledge the costs of its climate change policies can’t have helped.

Other factors might might have included the Coalition’s approach to infrastructure and to unions, which are generally regarded as business friendly.

Often traders react to what they think other traders will do rather than to anything fundamental. But it’s fair to say that, to start with, they were feeling good.

Mark Humphery-Jenner, Associate Professor of Finance, UNSW

This article is republished from The Conversation under a Creative Commons license. Read the original article.