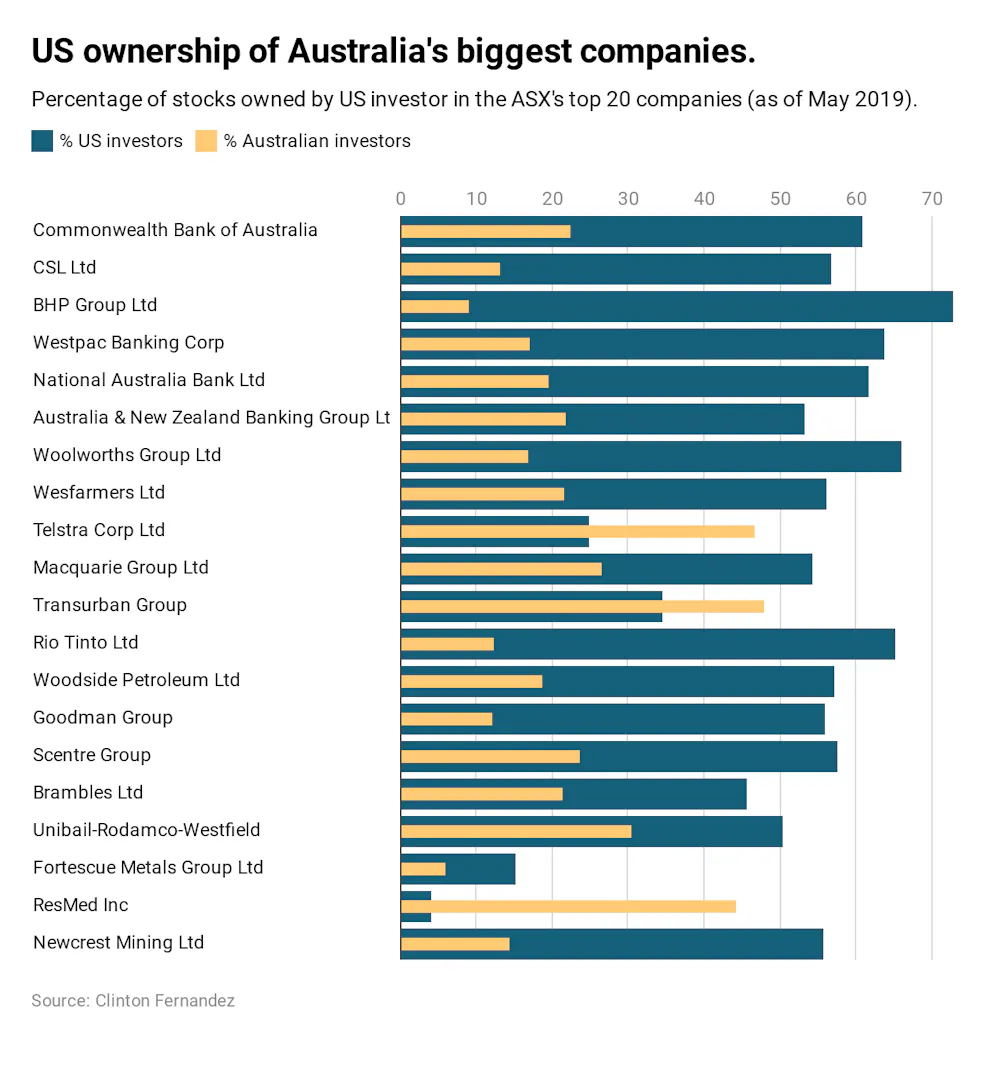

Worried about agents of foreign influence? Just look at who owns Australia's biggest companies

Most of Australia's biggest companies are majority-owned by US investors. This concentration of overt foreign influence should concern us.

Published on the 12 Sep 2019